Since our medical system began referring to itself as an industry, it has increasingly resembled a fast-food chain. While we continue to profess that patient safety is our top priority, the reality is that efficiency and quantity often take precedence over quality. When you only get 15 minutes with your primary care provider to discuss everything that has occurred since your last annual physical exam, there is no way your providers can truly understand you as a human being. At best, your doctor can identify any red flags that may necessitate further testing or treatment, possibly referring you to a specialist or prescribing medication, all the while hoping the issue will resolve itself. It is not uncommon that you have to reschedule another appointment to discuss further once the initial 15 minutes have elapsed. Why are you limited to just 15 minutes with your doctor? Why can’t your doctor address all your concerns in a single visit? There are numerous answers to these questions; however, the root of the problem lies in your medical bill.

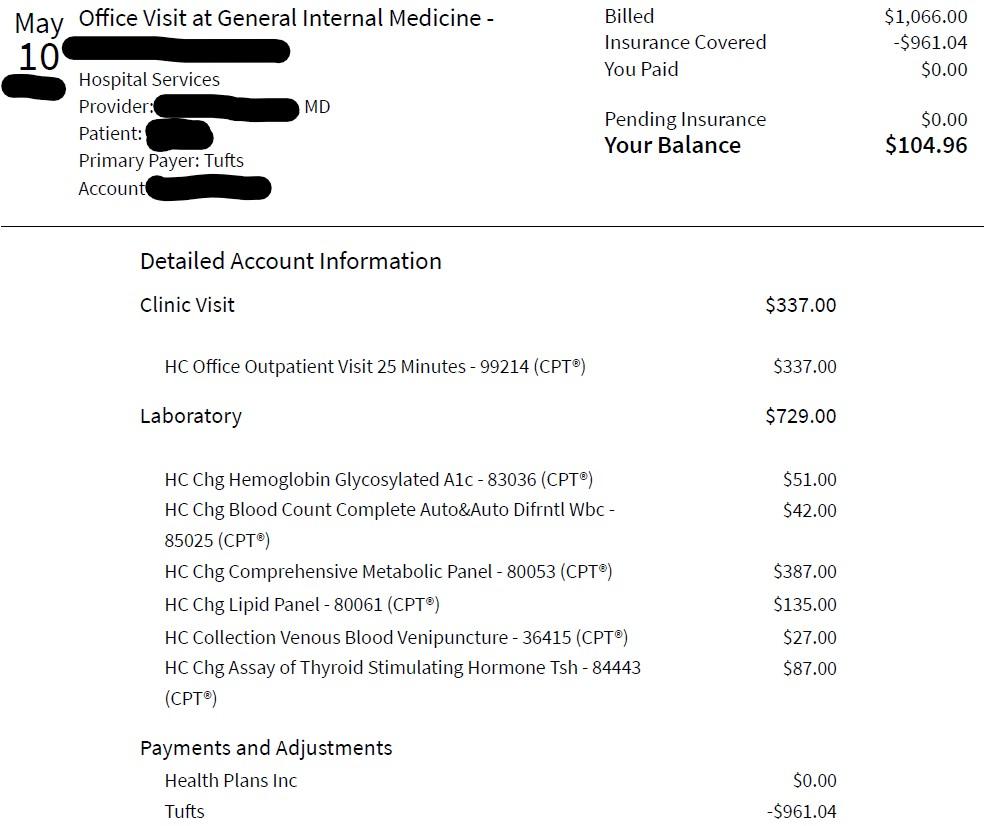

This is the medical bill(Fig.1) for my annual physical exam I received several weeks ago. It contains some basic information, and notably, the most crucial figure is the red number: $104.96. That is the amount that the hospital expects me to pay. As I reviewed the remaining items on the bill, I discovered that the total cost for this exam was $1,066, and $961.04 under Pmts/Adjs was deducted from the total. Pmts/Adjs stands for ‘payment/adjustment’, indicating the amount paid by the insurance. Typically, insurance companies have agreements with hospitals and providers. For certain services, your insurance only covers the contracted price, regardless of how much the provider bills. In this case, the hospital requested a payment of $1066, but the insurance company only approved $961.04. Sometimes, the provider may waive the difference between the total bill and the amount paid by the insurance. This practice is more common among small practice groups, as chasing down a hundred dollars may cost them more. In my case, the hospital has chosen to ask me to pay the remaining bill. If you were in my shoes, would you pay this bill?

Fig.1 Summary of Medical Bill

Before answering this question, you should first ask me three questions. What kind of services did I receive on that day? How does my insurance cover those services? Why did the insurance only partially pay the claim? First, I had an annual physical exam including some blood work, as part of preventative services. Secondly, my current health insurance has a deductible, which is the amount of money I need to pay before the insurance starts sharing the cost. However, for all preventative services, the deductible is not required, and the insurance provides 100% coverage.

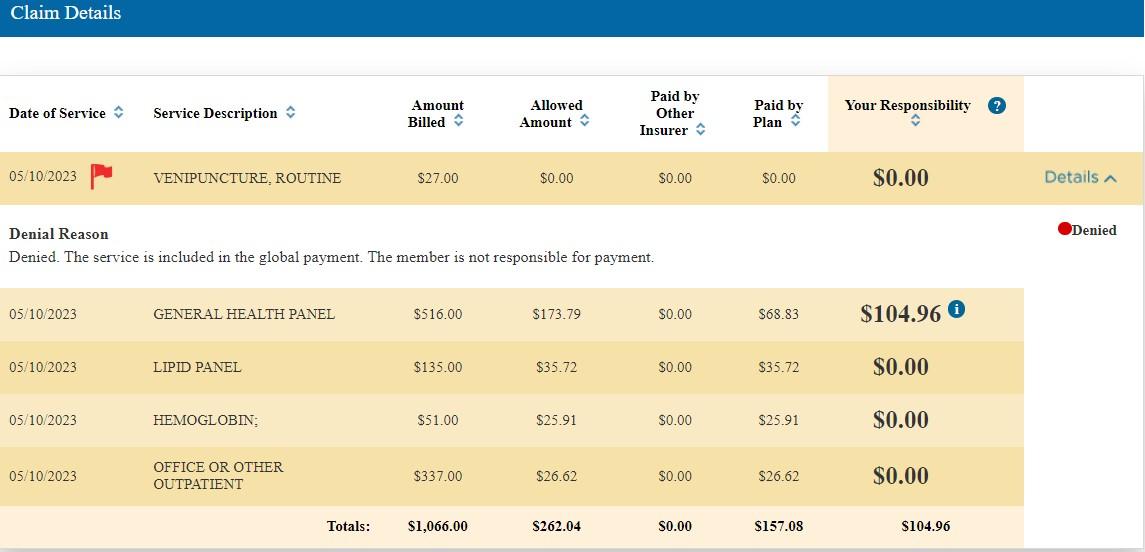

Now, there is a discrepancy between the total bill and the insurance payment. There are only two explanations. One is that the hospital is asking for too much money. If that is the case, the patient is not responsible for paying the excess amount. The hospital must adhere to the payment agreement with the insurance company since it receives payment from the insurance. You can find such an example in Fig.3. The hospital billed ‘venipuncture, routine’ for $27, and the insurance denied this service, noting ‘the member is not responsible for payment’. Another possibility is that the amount on the bill aligns with the payment agreement, but the insurance refused to pay for some of the services.

To sort this out, we need to examine the itemized medical bill(Fig.2). Remember you have the right to receive an itemized medical bill. You can contact the hospital or check your patient portal website for this information. Below is an example of my itemized medical bill. Before we dive in, let me explain what a CPT code is. CPT stands for Current Procedural Terminology, which is a standardized language for coding medical services and procedures for billing and reporting purposes. Each medical service or procedure has a unique CPT code.

On that day, I met with my primary care physician for approximately 25 minutes, categorized as an ‘office outpatient visit’. The CPT code 99214 indicates that my doctor spent 30-39 minutes on this visit. This timeframe encompasses not only the time the physician spent speaking with me face-to-face, but also the time she/he invested in documenting and reviewing my test results or medical records. When a provider spends an extended duration with a patient, they are required to use another CPT code to bill the insurance, allowing them to receive a higher payment. The value a provider generates within an 8-hour workday is determined by the total number of patients seen and the reimbursement for each visit. Through calculation, it becomes evident that a 15-20 minute visit is the most efficient from a profitability standpoint.

Returning to my medical bill(Fig.2), I underwent several blood tests on the same day, each with its unique CPT code. The hospital attempted to bill my former insurance company, Health Plan, inc, which denied the claim because I was not covered by the Health Plan at that time, resulting in a charge of $0. They subsequently billed Tufts Health Plan, which paid $961.04. Based on this itemized medical bill, it appears that the hospital accurately billed for all the services. So, why did the insurance decline to provide full payment?

Fig.2 Itemized Medical Bill

Fig.3 is the document I obtained from my insurance. If you have registered an online account on your health plan’s website, you should be able to find this information. It lists the services that the insurance approves and the corresponding reimbursement amounts. By comparing the hospital’s itemized bill with the insurance claim details, I discovered that ‘HC Chg Blood Count Complete Auto&Auto Difrntl Wbc’(85025), ‘HC Chg Comprehensive Metabolic Panel’(80053) and ‘HC Chg Assay of Thyroid Stimulating Hormone Tsh’(84443) were grouped together as ‘General Health Panel’(80050) on the insurance claim details. The insurance significantly reduced the charge for this service from $516 to $173.79 and only paid $68.83. After talking with the insurance representative, I was informed that this service was not covered according to their policy, and I would have to pay the deductible, which amounts to $104.96. However, they did cover the lipid panel and hemoglobin glycosylated A1c, because these two tests are considered ‘preventative services’.

If you have never reviewed your health insurance handbook, this explanation may seem reasonable. However, upon closer examination, something doesn’t add up. I went for an annual physical exam, during which no specific medical condition was addressed. My doctor ordered a series of tests to ensure my body’s overall health. All of these tests were blood tests. If the lipid panel and hemoglobin A1c are considered ‘preventative services’, why can’t the rest of blood tests be categorized the same way? In fact, ‘HC Chg Blood Count Complete Auto&Auto Difrntl Wbc’ examines different types of blood cells in your bloodstream; ‘HC Chg Comprehensive Metabolic Panel’ assesses major electrolytes, liver function, and kidney function; and ‘HC Chg Assay of Thyroid Stimulating Hormone Tsh’ is for evaluating thyroid function. These three tests are routinely conducted during annual wellness visits. So, what went wrong?

Fig.3 Insurance Claim Details

The problem lies in the fact that the hospital didn’t correctly bill these three blood tests. When the insurance receives a claim from the hospital, they initially examine CPT codes. If the combination of CPT codes aligns with their internal guidelines, the claim is approved, and the hospital is reimbursed. However, if a specific CPT code doesn’t match the service provided by the hospital, it raises a red flag. The insurance company will either deny the claim outright or request additional information for review. In my case, the insurance guidelines allow for reimbursement of CPT codes 83036, 80061, 85025, 80053 and 84443 during an annual wellness visit. However, the hospital didn’t submit each claim individually; instead, they substituted ‘80050’ for ‘85025’, ‘80053’ and ‘84443’. According to the insurance guidelines, ‘80050’ is not considered a ‘preventative service’, which is why the insurance company only made a partial payment, and I received a bill for the deductible.

Now, returning to the question, would you pay this bill? The answer is a resounding NO. The hospital needs to resubmit the claim with the appropriate CPT codes to the insurance company, and I anticipate that the insurance company will cover the entire claim.

Hospitals and insurance companies make mistakes frequently. Before making any payments, it is crucial not to blindly trust whatever the hospital or insurance company requests. Take the time to review the itemized bill, request individual CPT codes if they are not listed, confirm that the services billed match those you received, and always cross-reference your bill with the insurance claim history for any discrepancies.